THERE IS A BETTER WAY !

Catherine Austin Fitts

Dillion Read and Company, Inc. - The Aristocracy of Stock Profits

1, WHY I WROTE THIS STORY

I made the decision to write “Dillon, Read & Co. Inc. and the Aristocracy of Stock Profits” in the middle of a vegetable garden in Montana during the summer of 2005. I had come to Montana to develop a venture capital model to support a healthier, fresher local food supply. If we want clean water, fresh food, sustainable infrastructure, and healthy communities, we are going to have to finance and govern these resources ourselves. We cannot invest in the stocks and bonds of large corporations, banks and governments that are harming our food, water, environment and all living things and then expect these resources to be available when we need them.

Surviving and thriving as a free people depends on creating and transacting with currencies and  investments other than those printed and manipulated by Wall Street and Washington to the eventual end of our rights and assets.

investments other than those printed and manipulated by Wall Street and Washington to the eventual end of our rights and assets.

What I found in Montana, however, was what I have found in communities all across America. We are so financially entangled in the federal government and large corporations and banks that we cannot see our complicity in everything we say we abhor. Our social networks are so interwoven with the institutional leadership — government officials, bankers, lawyers, professors, foundation heads, corporate executives, investors, fellow alumni — that we dare not hold our own families, friends, colleagues and neighbors accountable for our very real financial and operational complicity. While we hate "the system," we keep honoring and supporting the people and institutions that are implementing the system when we interact and transact with them in our day-to-day lives. Enjoying the financial benefits and other perks that come from that intimate support ensures our continued complicity and contribution to fueling that which we say we hate.

Standing among the beautiful vegetables and flowers that Montana summer day, I was facing the futility of trying to craft investment solutions without some basic consensus about the economic tapeworm that is killing us and all living things — while we blindly feed the worm. In a world of economic warfare, we have to see the strategy behind each play in the game. We have to see the economic tapeworm and how it works parasitically in our lives. A tapeworm injects chemicals into a host that causes the host to crave what is good for the tapeworm. In America, we despair over our deterioration, but we crave the next injection of chemicals from the tapeworm.

With this in mind, I decided to write “Dillon Read & Co Inc. and the Aristocracy of Stock Profits” as a case study designed to help illuminate the deeper system. It details the story of two teams with two competing visions for America. The first was a vision shared by my old firm on Wall Street — Dillon Read — and the Clinton Administration with the full support of a bipartisan Congress. In this vision, America's aristocracy makes money by ensnaring our youth in a pincer movement of drugs and prisons and wins middle class support for these policies through a steady and growing stream of government funding and contracts for War on Drugs activities at federal, state and local levels. This consensus is made all the more powerful by the gush of growing debt and derivatives used to bubble the housing and mortgage markets, manipulate the stock and precious metals markets and finance trillions missing from the US government in the largest pump and dump in history — the pump and dump of the entire American economy. This is more than a process designed to wipe out the middle class. This is genocide — a much more subtle and lethal version than ever before perpetrated by the scoundrels of our history texts.

This case study provides a detailed example of the financial kickback machinery that makes the process go. It works something like this. A group of executives and investors start a company. Rather than build a business the old fashioned way, company profits are pumped up with government legislation, contracts, regulation, financing, subsidies and/or enforcement. This dramatically increases the value of the company's financial equity. The company and its initial investors then sell their stock at a profit. Such profits replenish contributions made to the kind of politicians who can arrange such government benefits. Such profits also fund philanthropy to foundations and universities that have large endowments that invest along side the investors. These tax-exempt organizations provide graduates to staff positions in the game, intellectual justification to attract popular support and photo opportunities which bestow legitimacy and social stature. Personnel cycle through the management and boards of business, government and academia, as real productivity falls and government deficits grow.

The second vision was shared by my investment bank in Washington — The Hamilton Securities Group — and a small group of excellent government civil servants and appointees who believed in the power of education, hard work and a new partnership between people, land and technology. This vision would allow us to pay down public and private debt and create new business, infrastructure and equity. We believed that new times and new technologies called for a revival that would permit decentralized efforts to go to work on the hard challenges upon us — population, environment, resource management and the rapidly growing cultural gap between the most technologically proficient and the majority of people. We believed that private and public capital should flow to that which was most economically productive rather than be mixed in a complex cocktail of insider deals designed to hollow out the American economy and culture.

My hope is that “Dillon, Read & the Aristocracy of Stock Profits” will help you to see the game sufficiently to recognize the dividing line between two visions. One centralizes power and knowledge in a manner that tears down communities and infrastructure as it dominates wealth and shrinks freedom. The other diversifies power and knowledge to create new wealth through rebuilding infrastructure and communities and nourishing our natural resources in a way that reaffirms our ancient and deepest dream of freedom.

My hope is that as your powers grow to see the financial game and the true dividing lines, you will be better able to build networks of authentic people inventing authentic solutions to the real challenges we face. My hope is that you will no longer invite into your lives and work the people and organizations that sabotage real change. If enough of us come clean and hold true to the intention to transform the game, we invite in the magic that comes in dangerous times.

Yes, there is a better way and, yes, we can create it.

|

[1] |

|

|||

|

I remember when John Birkelund first came to Dillon Read in 1981 to serve as President and Chief Operating Officer.[2] Dillon was a small private investment bank on Wall Street with a proud history and a shrinking market share as technology and globalization fueled new growth. I had joined the firm three years before and, after a period in corporate finance, had migrated to the Energy Group — helping to arrange financing for oil and gas companies who were clients of Birkelund’s predecessor, Bud Treman. Bud was a member of the old school — an ethical man increasingly frustrated with the corrupting influence of hot money and easy debt.

This was a time of transition. Dillon’s Chairman, Nicholas F. Brady, was considered one of George H. W. Bush’s most intimate friends and advisors. Both attended Yale, both were children of privilege. Bush had left his home in Greenwich Connecticut and with the help at his father’s networks at Brown Brothers Harriman had gone into oil and gas in Texas. Brady had gone to Harvard Business School and then returned to the aristocratic hunt country of New Jersey, where the Bradys and the Dillons had estates, to work at Dillon Read.

Bush climbed through Republican politics to become Director of the Central Intelligence Agency (CIA) during the Ford Administration. After spending four years displaced by the Carter Administration, Bush was now Reagan’s Vice President with Executive Order authority for the National Security Council (NSC) and U.S. intelligence and enforcement agencies. Bush’s new authority was married with expanded powers to outsource sensitive work to private contractors. Such work could be funded through the non-transparent financial mechanisms available through the National Security Act of 1947, and the CIA Act of 1949.

|

|||||

|

|||||

|

|||||

|

|||||

In April of 1981, Bechtel, working through the Bechtel private venture arm Sequoia, bought the controlling interest in Dillon Read from the Dillon family, led by C. Douglas Dillon, former U.S. Treasury Secretary[6] and son of the firm’s namesake, Clarence Dillon. This was a time when Bechtel was facing increased competition globally while experiencing a decline in the nuclear power business that they had pioneered.[7]

We found ourselves with new owners whose operations were an integral part of the military and intelligence communities and who had demonstrated a rapacious thirst for drinking from the federal money spigot.[8] George Schultz, former Secretary of the Treasury during the Nixon Administration, and now Bechtel executive, joined our board.

Unusual things started to happen that were very “un-Dillon-Ready-like.” First came a new bluntness. I will never forget the day that one of the partners brought around a very charming retired senior Steve Bechtel to tour the firm. Upon introduction, he peered up at me through thick glasses and said “Far out, a chick investment banker.” Then came strategic planning with SRI International, the think tank offshoot of Stanford University that had long standing relationships with the Bechtel family and Schultz. The head of the Energy Group that I worked for at the time was part of the planning group. His mood changed during this period and he later left the firm, retiring from the industry. Before going he warned me that I should do the same. He never said why…leaving a chill that I have felt many times since as ominous changes continue that have no name or a face.

|

The planning group recommended that we expand our business into merchant banking. This means managing money in venture investment by starting and growing new companies or taking controlling interests in existing companies, including “leveraged buy-outs.”[9] Rather than serving companies who needed to raise money by issuing securities, or make markets in existing securities, we were going to start raising money so we could create, buy and trade companies. A company was no longer a customer. They were now a target. Wall Street was its own customer who would raise money to buy companies who would work for us. This required new people with new skills.

|

John Birkelund arrived at Dillon Read in September 1981. Born in Glencoe, Illinois, he had graduated from Princeton and then had joined the Navy where he served with the Office of Naval Intelligence in Berlin. While in Europe he became friends with Edward Stinnes, who recruited him after a short career with Booz Allen in Chicago to work in New York for the Rothschild family, considered to be one of if not the wealthiest family in the world.[10] He started at Amsterdam Overseas Corporation, which then moved its venture capital business into New Court Securities with Birkelund as co-founder. New Court was owned by the Rothschild banks in Paris and London, Pierson Heldring Pierson in Amsterdam and the management. Their venture successes included Cray Research, inventor of the high-powered computers by that name, and Federal Express, the courier company based in Memphis which is the largest recipient of Federal government contracts in Tennessee. [11]

Birkelund was tall and energetic. He had piercing blue eyes, a driving and hard working ambition and intelligence. He seemed frustrated by the process of organizing and invigorating Dillon’s club-like culture. There was much about his willingness to try that endeared him to me — a point of view that was not reciprocated. Whatever the reason, I was not Birkelund’s cup of tea. I will never forget one of his early addresses to the banking group. He was full of energy and launched a section of his pep talk, “When you get up in the morning and look into the mirror to shave...” He suddenly froze, looking at me (one of few or possibly the only woman in the room) with fear that his reference to a masculine practice would offend. In the hopes of putting him at ease, I said with merriment, “Don’t worry, John, girls shave too.” The whole room burst out laughing and John turned red.

Birkelund had his hands full after arriving at Dillon Read. In 1982, Nick Brady left temporarily to serve in the U.S. Senate, appointed by Governor Tom Kean of New Jersey to serve out Harrison Williams term. George Schultz left Bechtel to serve as Secretary of State under Reagan. With Brady and Schultz in Washington D.C., the Bechtel relationship stalled. With Brady returning in 1983, Birkelund engineered the repurchase of the firm from Sequoia by the partners and the creation of meaningful venture and leveraged buyout efforts. In 1986, Brady and Birkelund lead the sale of Dillon Read to Travelers, the large Connecticut insurance company that later became part of Citigroup. The relationship with Travelers expanded our capital resources to participate in the venture capital and leveraged buyout businesses. In no small part thanks to Birkelund’s hard work and dictatorial cajoling, Dillon Read would not be left behind in the 1980s boom time. One of my favorite Dillon Read officers was the son of a former Dillon chairman and, thus, remarkably wise about the ways of the firm. I sought him out after a Birkelund temper tantrum and said that Birkelund was not at all like a “Brady Man” and that I was surprised at Nick’s choice. My colleague looked at me with surprise and said something to the effect of “Brady did not choose Birkelund. Birkelund is a 'Rothschild Man'.” I then said something about Dillon being owned by the Dillon partners, so what did the Rothschild’s have to do with us? My colleague rolled his eyes and walked away as if I was an interloper out of my league among the moneyed classes — clueless as to who and what was really in charge at Dillon Read and in the world. After all, even Time Magazine had declared that the Rothschild invasion of America was underway.[13] |

If you want to understand Dillon Read in the 1980s, you must understand R.J. Reynolds (RJR), a tobacco company based in Winston-Salem, North Carolina. According to the official Dillon history, The Life and Times of Dillon Read by Robert Sobel (Truman Talley Books/Dutton, 1991) at pages 345-346, RJR had been Dillon client for many years:

In 1984 and 1985, Dillon Read helped RJR merge with Nabisco Brands, making the combined RJR Nabisco one of the world's largest food processors and consumer products corporations. Nabisco’s Ross Johnson emerged as the President of the combined entity. Johnson preferred the bankers he had used at Nabisco — Lehman Brothers. Johnson was on the board of Shearson Lehman Hutton. To help RJR Nabisco digest the Nabisco acquisition, Dillon and Lehman helped to sell off eleven of RJR Nabisco’s businesses. In the process, numerous Lehman Brothers partners joined Dillon Read. Among them was Steve Fenster, who had been an advisor to the leadership of Chase Manhattan Bank and was on the board of American Management Systems (AMS), a company that figures in our story in the 1990s. After tours of duty in Dillon’s Corporate Finance and Energy Groups, I spent four years recapitalizing the New York City subway and bus systems on the way to becoming a managing director and member of the board of directors in 1986. I did not work on the RJR account. Odd bits of news would float back. They were always about the huge cash flows generated by the tobacco business and the necessity of finding ways to reinvest the gushing profits of this financial powerhouse. One of the young associates working for me teamed up with another young associate who worked on the RJR account to buy a sailboat in Europe. The second associate arranged to have the sailboat shipped to the U.S. through Sea-Land, an RJR subsidiary that provided container-shipping services globally. I was told RJR tore up the shipping bill as a courtesy. What kind of cash flows did a company have that could just tear up the shipping bill for an entire boat as a courtesy to a junior Dillon Read associate? I was to get a better sense of these cash flows many years later when I read the European Union’s explanation. The European Union has a pending lawsuit against RJR Nabisco on behalf of eleven sovereign nations of Europe who in combination have the formidable array of military and intelligence resources to collect and organize the evidence for such a lawsuit. The lawsuit alleges that RJR Nabisco was engaged in multiple long-lived criminal conspiracies. Excerpt From European Lawsuit Against RJR Nabisco If you like spy novels, you will find that the European Union’s presentation of fact to be far more fascinating than fiction. One of the complaints filed in the case describes a rich RJR history of business with Latin American drug cartels, Italian and Russian mafia, and Saddam Hussein’s family to name a few. The Introduction reads as follows:

The European Union goes on to explain the role of cigarettes in laundering illicit monies:

Particularly endearing, the European Union alludes to one of the most important secrets of money laundering — that the attorney-client privilege of lawyers and law firms, particularly the most prestigious Washington and Wall Street law firms, are a preferred method for the communication of corporate crimes:

More information on the RJR and other tobacco company lawsuits is provided at the Resource Page at this website. The reader can access directly by linking through this footnote.[13d] You will find an update in the litigation section in the SEC annual report for 2004 for RJR’s successor corporation, Reynolds American, as well as other updates on litigation cases involving smuggling and slavery reparations.[14] According to Dillon Read, the firm’s average return on equity for the years 1982-1989 was 29%. This is a strong performance, and compares to First Boston, Solomon, Shearson and Morgan Stanley’s average returns of 26% , 15%, 18% and 31% respectively.[15] Given what we now know from the European Union’s lawsuit and other legal actions against RJR Nabisco and its executives, this begs the question of what Dillon’s profits would have been if the firm had not made a small fortune reinvesting the proceeds of — if we are to believe the European Union — cigarette sales to organized crime including the profits generated by narcotics flowing into the communities of America through the Latin American drug cartels. To understand the flow of drug money into and through Wall Street and corporate stocks like RJR Nabisco during the 1980s, it is useful to look more closely at the flow of drugs from Latin America during the period — and the implied cash flows of narco dollars that they suggest. Two documented situations involve Mena, Arkansas and South Central Los Angeles, California. |

During the 1980s, a sometime government agent named Barry Seal led a smuggling operation that delivered a significant amount of narcotics estimated to be as much as $5 billion from Latin America through an airport in Mena, Arkansas.[16] According to investigative reporters and researchers knowledgeable about Mena, the operation had protection from the highest levels of the National Security Council then under the leadership of George H.W. Bush and staffed by Oliver North. According to investigative reporter and author Daniel Hopsicker, when Seal was assassinated in February 1986, Vice President George H.W. Bush’s personal phone number was found in his wallet. Through Hopsicker's efforts, Barry Seal’s records also divulged a little known piece of smuggling trivia — RJR executives in Central America had helped Seal smuggle contraband into the U.S. in the 1970s.[17]

|

An independent counsel was appointed to investigate the concerns raised by Hassenfuss’ capture. As described in my article, "The Myth of the Rule of Law," the founders note written by Chris Sanders, head of Sanders Research states:[19]

“The investigation resulted in no fewer than 14 individuals being indicted or convicted of crimes. These included senior members of the National Security Council, the Secretary of Defense, the head of covert operations of the CIA and others. After George Bush was elected President in 1988, he pardoned six of these men. The independent counsel’s investigation concluded that a systematic cover up had been orchestrated to protect the President and the Vice President… During the course of the independent counsel’s investigation, persistent rumors arose that the administration had sanctioned drug trafficking as well as a source of operational funding. These charges were successfully deflected with respect to the independent counsel’s investigation, but did not go away. They were examined separately by a Congressional committee chaired by Senator John Kerry, which established that the Contras had indeed been involved in drug trafficking and that elements of the U.S. government had been aware of it.”

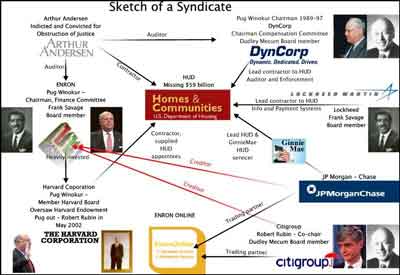

There is a standard line you hear when you try to talk to people in Washington, D.C. about the flood of narcotics operations and money laundering in Arkansas during the 1980s. “Oh, those allegations were entirely discredited,” they say. This is not so. Thanks to numerous journalists and members of the enforcement community, the documentation on Mena drug running and the related money laundering is quite serious and makes the case that the government was engaged or complicit in significant narcotics trafficking. This includes the various relationships to employees of the National Security Council, the Department of Justice and the CIA under Vice President Bush’s leadership and to then Governor of Arkansas, Bill Clinton and a state agency, the Arkansas Development and Finance Agency (ADFA). ADFA was a local distributor of U.S. Department of Housing and Urban Development (HUD) subsidy and finance programs and an active issuer of municipal housing bonds. One of its law firms included Hillary Clinton and several members of Bill Clinton’s administration as partners, including Deputy White House Counsel Vince Foster and Associate Attorney General Webster Hubbell.

Those convicted and pardoned by President Bush included former Bechtel General Counsel, Harvard trained lawyer Cap Weinberger who as Secretary of Defense had presided over one of the most crime-ridden government contracting operations in U.S. history.[20] Forbes editor James Norman left Forbes in 1995 as a result of Forbes refusal to publish his story “Fostergate,” about the death of Vince Foster and its relationship to the sophisticated software, PROMIS, allegedly used to launder money, including funds for the arms and drugs transactions working through Arkansas. Norman’s story allegedly implicated Weinberger in taking kickbacks through a Swiss account from Seal’s smuggling operation. In other stories, the software was considered to be an adaptation of PROMIS software stolen from a company named Inslaw and turned over to an Arkansas company controlled by Jackson Stephens. An historical footnote to our story is that a later study of the prison industry shows that Jackson Stephens’ investment bank, Stephens, Inc., was the largest issuer of municipal bonds for prisons.

Some of the most compelling documentation on Seal’s Mena operation and related money laundering was provided by William Duncan, the former Special Operations Coordinator for the Southeast Region of the Criminal Investigation Division, Internal Revenue Service at the U.S. Treasury. The U.S. Treasury fired Duncan in June of 1989 when he refused to dilute or cover up the facts in Congressional testimony.[21] [22]Since it is illegal to lie to Congress, this is the equivalent of being fired for refusing to break the law, and in the process, protecting a criminal enterprise.

The Secretary of the Treasury when Duncan was fired was Nicholas F. Brady, former Chairman of Dillon Read. Brady left Dillon in September 1988 to join the Reagan Administration in anticipation of Bush’s victory in the November elections. Duncan was fired within months of two important events detailed later in the story:

(i.) the RJR Nabisco takeover made famous by the book, Barbarians at the Gate: The Fall of RJR Nabisco by Brian Burrough and John Helyer (Harper & Row, 1990) as well as a later movie by the same name, and

(ii.) Lou Gerstner, now chairman of the Carlyle Group, joining RJR Nabisco to make sure that the aggressive management was in place to pay back billions of new debt issued in the takeover.

As we will see later in our story, the inability to stop Duncan from documenting the corruption at Mena and the U.S. Treasury, emphasized the importance of placing control of the IRS and its rich databases and information systems which illuminated flows of money in friendlier hands.

Narco Dollars in the 1980s — South Central, Los Angeles

|

Gary Webb’s "Dark Alliance" story documenting the explosion of cocaine coming from Latin America into South Central Los Angeles during the 1980s was originally published by the San Jose Mercury News in the summer of 1996 and then published in book form in 1998. The story and its supporting documentation was persuasive that the U.S. government and their allies in the Contras were involved in narcotics trafficking targeted at American children and communities.

All the usual suspects did their best to destroy Webb’s credibility and suppress his story. This included the Washington Post, which had pulled Sally Denton and Rodger Morris’ story on Mena at the last minute in 1995 — leaving it to run later in the summer in Penthouse Magazine. Luckily, Webb had arranged to have significant amounts of legal documentation substantiating his story posted on the San Jose Mercury News website. By the time that the News was pressured to take the story down, thousands of interested people all over the world had downloaded overwhelming evidence. Thanks to the Internet, the crack cocaine Humpty Dumpty could not be put back together again.

In response to citizen concern inspired by Webb's story, then Director of the CIA, John Deutsch, agreed to attend a town hall meeting in South Central Los Angeles with local Congressional representatives in November 1996. Confronted by allegations in support of Webb's story, Deutsch promised that the CIA Inspector General would investigate the "Dark Alliance" allegations.

This resulted in a two volume report published by the CIA in March and October of 1998 that included disclosure of one of the most important legal documents of the 1980s — a Memorandum of Understanding (MOU) between the Department of Justice (DOJ) and the CIA dated February 11, 1982 in effect until August 1995.[23] At the time it was created, William French Smith was the U.S. Attorney General and William Casey, former Wall Street law partner and Chairman of the SEC was Director of the CIA. Casey, like Douglas Dillon, had worked for Office of Strategic Services (OSS) founder Bill Donovan and was a former head of the Export-Import Bank. Casey was also a friend of George Schultz. Bechtel looked to the Export-Import Bank to provide the government guarantees that financed billions of big construction contracts worldwide. Casey recruited Stanley Sporkin, former head of SEC Enforcement, to serve as general counsel of the CIA. When Schultz joined the Reagan Administration as Secretary of State, such linkages helped to create some of the personal intimacy between money worlds and national security that make events such as those which occurred during the Iran Contra period possible.

|

No history of the 1980s is complete without an understanding of the lawyers and legal mechanisms used to legitimize drug dealing and money laundering under the protection of National Security law. Through the MOU, the DOJ relieved the CIA of any legal obligation to report information of drug trafficking and drug law violations with respect to CIA agents, assets, non-staff employees and contractors.[23] Presumably, this included the corporate contractors who, by executive order, were now allowed to handle sensitive intelligence and national security outsourcing.

With the DOJ-CIA Memorandum of Understanding, in effect from 1982 until rescinded in August 1995, a crack cocaine epidemic ravaged the poorer communities of America and disenfranchised hundreds of thousands of poor people into prison who, now classified as felons, were safely off of the voting roles. Meantime, the U.S. financial system gorged on what had grown to an estimated $500 billion-$1 trillion a year of money laundering by the end of the 1990s. Not surprisingly, the rich got richer as corporate power and the concentration of investment capital skyrocketed on the rich margins of state sanctioned criminal enterprise.

Yale Law School trained Stanley Sporkin was appointed by Reagan in 1985-86 to serve as a judge in Federal District court, leaving the CIA with a legal license to team up with drug dealing allies and contractors. From the bench many years later, he helped engineer the destruction of my company Hamilton Securities while preaching to the District of Columbia bar about good government and ethics. He retired from the bench in 2000 to become a partner at Weil, Gotshal & Manges, Enron's bankruptcy counsel.

Gary Webb died in 2004, another casualty of an intelligence, enforcement and media effort that keeps global narcotics trafficking and the War on Drugs humming along by reducing to poverty and making life miserable for those who tell the truth. At the heart of this machinery are thousands of socially prestigious professionals like Sporkin who engineer the system within a labyrinth of law firms, courts and government depositories and contractors operating behind the closely guarded secrets of attorney client privilege and National Security law and the rich cash flows of the U.S. federal credit.[24]

Leveraged buyouts were a phenomenon that got going in the 1980s. A leveraged buyout (LBO) is a transaction in which a financial sponsor buys a company primarily with debt — effectively buying the target company with the target's own cash and financial ability to service the debt. As described in Barbarians at the Gate: The Fall of RJR Nabisco at pages 140-141 :

“In 1982 an investment group headed by William Simon, a former treasury secretary, took private a Cincinnati company, Gibson Greetings, for $80 million, using only a million dollars of its own money. When Simon took Gibson public 18 months later, it sold for $290 million. Simon’s $330,000 investment was suddenly worth $66 million in cash and securities… By 1985, just two years after Gibson Greetings, there were 18 separate LBO’s valued at $1 billion or more. In the five years before Ross Johnson [RJR Nabisco Chairman and CEO] decided to pursue his buyout, LBO activity totaled $181.9 billion, compared to $11 billion in the six years before that.

In a highly leveraged company, the equity owner does not really have control. It’s the bondholder or creditor who can put the company in default. With the dirty tricks available from covert "economic hit" teams combined with a creditor's ability to throw a company in default, who needs to be a visible owner? Unmentioned was the ease and elegance with which junk bonds made it possible to take over companies with narco dollars and other forms of hot money financed by powerful partners hidden behind mountains of debt. There emerged a growing number of attractive business savvy investment firms vying to be the owners of record for a growing number of companies taken private in leveraged buyouts. This included Kohlberg Kravis Roberts & Co. (KKR), the LBO firm that took over RJR Nabisco in 1989 in one of the most visible takeovers of the decade, documented by Barbarians at the Gate. Dillon Read represented the RJR Nabisco board on the transaction. While the bidding war between KKR and the management group led by Ross Johnson teamed with Shearson Lehman escalated, I remember being dumbfounded as to why anyone thought that RJR Nabisco could service the proposed amounts of debt. In later years as I read reports that the debt was being serviced, I wondered what magic tricks KKR had that we mere mortals were missing. In reading Barbarians at the Gate, it turns out they managed to win despite not having the highest bid on all bidding rounds. One wonders the extent to which the bidding process was reengineered to ensure a KKR win and the media manipulated to make it look like the board had reasons to favor KKR over management other than the real reasons. Years later, reading between the lines of the European Union lawsuit, it struck me that perhaps KKR had simply sheltered one of the worlds premier money laundering networks and, behind the veil of a private company, taken this network to a whole new level. In that same period, they recruited Lou Gerstner from American Express to run the more aggressive, more leveraged RJR. The lawsuits filed by the European Union against RJR allege that top management, including during the time Gerstner led the company as CEO, directed RJR’s illegal activities. When the European Union said “highest corporate level” and “officers and directors,” that meant Lou Gerstner — and through Gerstner and the board, the controlling shareholder, KKR. Successful at RJR, Gerstner left to revitalize IBM and was then knighted by Queen Elizabeth. After retiring from IBM, Gerstner was chosen to chair the Carlyle Group in Washington in late 2002. The European Union’s lawsuit highlights Gerstner’s deeper qualifications to revitalize IBM, one of the most powerful military and intelligence contractors, and to lead an LBO firm like Carlyle that built its business on military and intelligence contractors and the intelligence to which such contractors are privy.[25] Henry Kravis and George Roberts were two of the founders of KKR. Kravis’ father — successful in the Oklahoma oil and gas business — was reported to be a friend of the Bush family and had many close ties with Wall Street. Henry Kravis and his San Francisco cousin and partner, George Roberts were said to be generous supporters of the Bush campaign.

It was inconceivable to me that KKR could have won the RJR Nabisco bidding war despite lower bids without Vice President George H. W. Bush in the White House (having just won the election) and/or Nick Brady at Treasury exercising their invisible hand. Bush’s White House counsel, Harvard educated C. Boyden Gray (now partner at Wilmer Cutler) was heir to one of the many North Carolina RJR fortunes. When the bidding team led by Ross Johnson, then CEO of RJR Nabisco lost to KKR, I wondered, did Nick finally get Ross Johnson back for diluting Dillon Read’s RJR lead underwriting business after the merger with Nabisco in 1985? When Nick Brady first got to Treasury, he was apparently slow to staff and organize his public affairs office. Before leaving Wall Street in April of 1989 to join the Bush Administration, I used to get calls from reporters looking for basic background, including his bio. One reporter asked me if I thought Brady was tough enough to survive in Washington’s treacherous waters. I responded that, “Yes, Brady did have a genteel manner. However, the world was littered with the bodies of the men and women who had underestimated Nick Brady.” |

There was an invisible spirit that crept through our lives on Wall Street in the 1980s. LBO’s were a part of it. I could never quite put my finger on what was wrong. It was as if there was too much dirty money and, as it grew more and more powerful in invisible ways, the way companies were financed, bought and sold grew progressively more out of control. The common sense and humanity seemed to drain out, and as personal wealth of the insiders grew, so did the lies.

For example, when the Dillon Read partners sold the firm in 1986 to Travelers, three years after buying our stock back from Bechtel, Birkelund came to my office to ask me what I thought of the deal. I told Birkelund that it was a done deal and that my opinion as one of the newest partners was irrelevant. Birkelund insisted — he really wanted to know. I told him that I was disappointed that we were no longer owners and that I thought a large insurance company would not prove to be a good business fit. He exploded with rage and stomped out of the office. Minutes later, my husband Geoffrey — a successful Wall Street attorney — called to tell me that he had just had a call from Fritz Hobbs, one of the senior Dillon partners, saying that Birkelund told him that I had resigned from the firm and that he, Geoffrey, needed to exercise some control of his wife. I explained that I had not resigned. I then advised Geoffrey to call Fritz and persuade him that he had managed to get me under control, to assure him that I had not and had no intention of resigning and that he, Geoffrey, could be counted on to make sure that I supported the sale and the changes contemplated. Hence, my partners could look to my husband to manage me. I then spent several weeks collaborating with Geoffrey on the manipulation of me — which turned out to be a remarkably effective, though unorthodox, communication vehicle. My back channel[26] was compromised several weeks later when Ken Schmidt, the head of Dillon’s municipal department who Birkelund had also assigned to “manage” me while I managed a large and profitable client and deal flow, broke down one night after several drinks and confessed that he and my other partners were using my husband to manipulate me. Perhaps he would not have felt as guilty if he realized where Geoffrey was accessing his strategies.

After the sale of Dillon to Travelers, we put together significant Travelers financial support for our LBO business. Birkelund called me to his office to ask me if I would take the lead on marketing our LBO’s to bond buyers. This request caught me off guard, as I was confident that this was a role in which I would not be successful. I asked why he thought I was appropriate. He described my success at designing and marketing $4 billion of New York City transportation systems bonds. This was a deal that nine firms had said could not be done but that had gotten done quite successfully with Dillon Read’s leadership, making the first page of the New York Times and the financial press. I explained to John that I could sell deals that I had personally structured and which I believed to be sound credits because they were based on some fundamental wealth-creating purpose that would ensure the bond buyers were paid back. However, a lot of the LBOs flowing through Wall Street were not based on sound financial engineering and involved companies that were of dubious value. I was terrific with Dillon’s investment clients when I believed in a credit. Unless I was personally confident in the investments long-term viability, I was not effective at selling it. John thought I was being difficult and I was amazed that he could not understand that just as fish don’t fly, I did not have the ability to do a good job for the firm at this task. It was as if two parallel universes were trying to communicate and failed. One was looking to go with the flow of more and more government and corporate debt without thought for how future generations would pay back all this debt — what some of us called the debt bubble — because that was the way to win at the game of hot money profits. The other thought that money served a strategic purpose and that flipping people and companies like pancakes for quick profits was risky business. Things came to a head when I arrived at the weekly banking meeting of the Dillon Read partners one morning in 1988 and listened to Steve Fenster, one of the partners who had joined us in 1987 from Lehman Brothers with an interim stint at Chase, make his presentation on why Dillon’s LBO group should take the second position behind First Boston in the Campeau hostile takeover of the Federated Department Stores.[27] During his presentation, Fenster, later a professor at the Harvard Business School, presented a “sources and uses of funds” statement. This is a statement that estimates where the money is coming from to buy the company and how it will be spent and in what amounts. Steve described a significant source of funds would come from “productivity improvements” — a portion of what was needed to fund the cost of hundreds of millions for golden parachutes for senior management and fees for lawyers and investment bankers. The “productivity improvements” were the increased profits to be generated by middle management over many years — all without partaking of the hundreds of millions pork fest enjoyed up front by senior management and Wall Street. We would get rich and get out up front. The guys in the trenches would work like dogs for years for scraps if the deal were to work. I was stunned. I asked Steve why in the world middle management would stick around and spend years working to generate increased profits without adequate incentives. After all, these financials would be disclosed in SEC filings. The companies’ middle managers would read the proxy and could “walk with their feet.” This meant the company would fail. If the company failed before we sold new bonds, the Travelers bridge line that we were using would lose millions. If it failed after we sold the bonds, our customers who bought the bonds would get left holding the bag. Fenster looked at me in disgust and said something to the effect of “we will be out in December,” meaning if the deal tanks it will be someone else’s problem. I responded "Steve, our bond buyers won’t be,” meaning that Dillon would be selling the securities to pension and mutual funds and other bond buyers who would then take what could be millions in losses. By this time, Brady had left for Washington and Birkelund was now in command of the firm. Birkelund was trying to build a fortune. Nick had one to protect. It struck me that the balance that the Brady-Birkelund partnership had somehow managed to strike between playing to win in the hot money game and not putting Brady’s personal reputation at risk was gone. Dillon anticipated significant fees and Fenster and the partners around the table were hungry for the quick bucks of big year-end bonuses. That was when I decided that we might be losing sight of the line between financial engineering and financial fraud. I left the boardroom and headed downstairs to make a call to Washington, D.C. There was nothing else to learn at Dillon Read. It was time to go — I was too much a member of the old school. Other firms had indicated an interest in recruiting me. However, I had promised Nick I would institutionalize my clients and not strip the business from the firm. The way to continue to do that was to join the incoming Bush Administration in Washington, D.C. The corruption was bad, a crash was coming and Washington would lead the clean up. Besides, the corruption was being engineered in part through Washington. I wanted to understand how the economy and markets really worked. It was long my dream to find ways that investors could profit from activities which increased human and environmental safety and wealth. I needed to understand how the federal government and credit worked. When the Federated Department Stores declared bankruptcy on January 15, 1990 as a result of their takeover by Campeau using an unsound financial structure, Dillon Read, Travelers and Dillon’s bond buyers were left holding millions of badly discounted securities. By that time, I was Assistant Secretary of Housing-FHA Commissioner at HUD managing billions of defaulted mortgages and coordinating with the group at the Resolution Trust Corporation who were managing billions of defaulted savings and loan (S&L) mortgages. While Birkelund and Fenster were explaining the Campeau-Federated defaults to Travelers, I was learning why Oliver North allegedly referred to HUD as “the candy store of covert revenues.”[28] It took years of cleaning up the mortgage mess to understand that this homebuilding and mortgage fraud was an integral part of the National Security Council’s shenanigans during Iran-Contra and a U.S. federal debt that was growing at alarming rates. |

When I told Nick Brady in 1989 that I was going to work at HUD, he said, “You can’t go to HUD — HUD is a sewer.” While my experience as Assistant Secretary cleaning up significant mortgage fraud that lost the government billions during the 1980s confirmed that HUD’s financial reputation was deserved, leading the FHA provided invaluable insight into how government management of the economy one neighborhood at a time really harms communities. Hence, access to the “real deal” on real estate and the mortgage markets was an opportunity. If you want to see the real economy in a place, you absolutely want an accurate map of the financial flows in that system — starting with the land and real estate. My favorite description of HUD was to come many years later from staff to the Chairman of the Senate HUD appropriation subcommittee — Senator Kit Bond. When asked what was going on at HUD, the Congressional staffer said, “HUD is being run as a criminal enterprise.”[29]

Shortly after arriving at HUD in April 1989, I began to learn about the FHA Coinsurance program. Since 1984, HUD/FHA had allowed private mortgage bankers to issue federal credit to guarantee multi-family apartment projects. After issuing $9 billion in mortgage guarantees, HUD/FHA was to lose something approaching 50% of the value of the portfolio — a level of losses hard to explain with mortal logic. When my staff approached me with a proposal to bail out a mortgage company so they could continue to lose money for us, I asked why we should spend money to lose more money in a way that would harm communities. After a long silence during which 30 staff members intently studied their feet, one brave soul explained to me that the mortgage bank was owned and run by a major Republican donor. Shocked, I said. “I am a major Republican donor,” and pointing to my presidential cufflinks that were adorning my French cuffs, “I got a pair of cuff links. You get cuff links. You don’t get $400 million of federal credit to throw down the drain.” My staff looked at me like I was so naive and clueless that there was no point in trying to communicate with me — better to let me learn the hard way.

In the process of cleaning up the coinsurance portfolio, I got a chance to learn more about some of the tax-exempt housing bond deals that involved FHA mortgage insurance. Examples of these deals were those done through one of the Connecticut state housing authorities by a Dillon Read banker, Jewelle Bickford, during the 1980s. Bickford had a lot of support from two of the largest future Dillon Read investors in Cornell Corrections — Ken Schmidt and Birkelund — which was hard for me to fathom. Bickford was one for shortcuts and what sounded to me like more than little white lies. Schmidt shared an intelligence background with Birkelund. He served with Air Force Intelligence early in his career as Birkelund had served in the Office of Naval Intelligence (ONI). When I later realized the role of the intelligence agencies in the HUD portfolio their comfort with HUD deals in Connecticut with high default rates seemed somehow more logical.

For comparisons sake, $4 billion is about the amount of money that would buy you a controlling lead position in taking over one of the world’s premiere money laundering networks. When KKR raised the war chest in 1987 that gave them the wherewithal to bid and win RJR Nabisco, it amounted to $5.6 billion. Money is like the Pillsbury Doughboy. When you squeeze down on one part, it pops up someplace else. Wall Street Lessons: Dillon Read’s James Forrestal

Shortly after resigning from government, Forrestal died falling out of a window of the Bethesda Naval Hospital outside of Washington, D.C. on May 22, 1949. There is some controversy around the official explanation of his death — ruled a suicide. Some insist he had a nervous breakdown. Some say that he was opposed to the creation of the state of Israel. Others say that he argued for transparency and accountability in government, and against the provisions instituted at this time to create a secret “black budget.”[32] He lost and was pretty upset about it — and the loss was a violent one. Since the professional killers who operate inside the Washington beltway have numerous techniques to get perfectly sane people to kill themselves, I am not sure it makes a big difference. Approximately a month later, the CIA Act of 1949 was passed. The Act created the CIA and endowed it with the statutory authority that became one of the chief components of financing the “black” budget — the power to claw monies from other agencies for the benefit of secretly funding the intelligence communities and their corporate contractors. This was to turn out to be a devastating development for the forces of transparency, without which there can be no rule of law, free markets or democracy. I studied Forrestal’s oil painting with his solemn stare during many a private lunch — each time reminded that government service was an important duty and honor in the Dillon tradition but it was a dangerous business. Congressional Committees had roughed up Clarence Dillon. Forrestal had died. Douglas Dillon was Secretary of the Treasury when Kennedy was assassinated. Because I wanted to understand how the world really worked, I listened carefully. Over years of private lunches and dinners and conversations I watched and listened to hundreds of lessons on how to be careful — the tricks of predator evasion in Wall Street and Washington. In the midst of many knowledgeable teachers, Forrestal’s leadership was a guiding light that was to serve me well in the years ahead. Wall Street Lessons: The Power of the PeopleAnother thing I learned on Wall Street is the extent to which those who appear to have little material power can have significant power when they organize to do so. My rise to partnership at Dillon Read was fueled by a steady stream of intelligence from loyal secretaries, print shop personnel, drivers and staff whose generosity, street smarts and hard work was a constant reminder that the rise to Wall Street’s board rooms was not necessarily based on performance as opposed to privilege. One of the greatest challenges as an associate at Dillon Read was knowing where to invest our time when multiple partners were pressing us to give priorities to their projects. Hence, a heads up from someone’s secretary that they were trashing me in the year-end reviews was insider intelligence worth its weight in gold. Giving first priority to those who supported us in year-end reviews and compensation could be the difference between failure and success. Right after I became a partner, I got a call from a personnel department director who was looking for a new secretary for me. The person who called said they were interviewing someone who has been with a Canadian Broadcasting office in New York for seventeen years. This was her first interview since they shut the office down. She was absolutely excellent and if we wanted to recruit her we needed to make her an offer right away. The personnel director said, “The only problem is that she is Jamaican (of African descent), but she is very light skinned.” I was stunned and said something to the effect of “Who cares?” The personnel person said, “If I sent a black person to be interviewed with most of the partners in this firm, I would be fired.” And so I hired Pat Phillips to work for me and was the beneficiary of her extraordinarily overqualified talent until her death twelve years later, by which time she was a Hamilton shareholder and Secretary of our board. Many years later, after I had started my own investment bank in Washington, D.C., I got a call from a driver at one of the car services that we used to use when I was at Dillon. He said, “Are you doing a deal with Ken Schmidt?” I explained that, yes, I had proposed working together on a fairly large complex transaction. It would take a lot of work but if successful would be great business for both firms. The driver said, “He was in the car last night. He was bragging about how he was going to screw you. Here is what he is going to do.” This was the same Ken Schmidt who had confessed the Dillon partners conversations with my ex-husband. Ken was still blubbering indiscreetly about his bad deeds. And so the driver saved me from my mistake of attempting to partner with my old firm. |

After Bickford’s housing bonds were embroiled in the coinsurance crash and burn, Jewelle somehow managed to get promoted up — landing at Birkelund’s old firm, Rothschild Inc. Which always made me wonder exactly whose bank accounts ended up with the $4 billion emptied out of the FHA mutual funds at HUD as a result of coinsurance, not to mention the billions more lost in the single family FHA programs. Over $2 billion was lost by FHA/HUD in the Texas region in fiscal 1989 alone. The Texas region had included Arkansas, where the state agency, ADFA was so bad they had been disqualified at one point according to the HUD Fort Worth regional leadership. It was this state agency which was alleged to have laundered the local profit share of the arms and drug trafficking channeled through Mena, Arkansas.

After Bickford’s housing bonds were embroiled in the coinsurance crash and burn, Jewelle somehow managed to get promoted up — landing at Birkelund’s old firm, Rothschild Inc. Which always made me wonder exactly whose bank accounts ended up with the $4 billion emptied out of the FHA mutual funds at HUD as a result of coinsurance, not to mention the billions more lost in the single family FHA programs. Over $2 billion was lost by FHA/HUD in the Texas region in fiscal 1989 alone. The Texas region had included Arkansas, where the state agency, ADFA was so bad they had been disqualified at one point according to the HUD Fort Worth regional leadership. It was this state agency which was alleged to have laundered the local profit share of the arms and drug trafficking channeled through Mena, Arkansas.

According to a later Harvard case study on Cornell’s facility,[34] David Cornell was pursuing the prison business while at Becon in partnership with Dillon Read — presumably the part of the firm that helps to create and sell the types of local government bonds that finance many prisons. When Becon decided not to pursue the prison business, Cornell decided to leave and start his own private prison company. With Bechtel out of the business, Cornell and Dillon then decided to use Brown & Root to construct the first prison. Brown & Root was a subsidiary of Halliburton, both based in Houston like Cornell Corrections. According to Cornell’s filings with the SEC and other corporate reports, Dillon used funds from three of its venture funds, Concord, Concord II and Concord Japan to make these initial investments. Dillon Read’s April 1997 SEC filing described Concord and Concord II as limited partnerships organized under the laws of New York and Delaware.

To understand Dillon’s investments in Cornell it is essential to understand who governed Dillon Read, who at Dillon invested personally as well as who at Dillon along with outside directors helped to govern the Dillon venture funds that invested in Cornell. These are the people who are responsible for the investment decisions and who would have benefited in various forms. As provided in Dillon’s Cornell SEC filings, Dillon, Read Holding Inc.,[35] Dillon, Read Inc.[36] and Dillon, Read & Co. Inc.[37] listed their officers and directors as including John P. Birkelund, David W. Niemiec, Franklin W. Hobbs, IV, Francois de Saint Phalle as well as senior leadership from Barings, the British bank that was now an investor in Dillon and ING, the Dutch financial conglomerate that acquired Barings when it failed in 1995.[38] The presence of Barings in Dillon’s governance structure is noteworthy. Barings, the oldest merchant bank in England and said to be a financial leader in the 1800s China opium trade, collapsed in February 1995 as a result of a trading scandal in Asia and was taken over by ING. Barings became the lead outside investor in Dillon Read in late 1991, when they effectively financed Dillon’s management buying out Travelers. This was the same year that Dillon bankrolled Cornell Corrections. Barings’ difficulties in 1995 may have increased the pressure on Dillon to generate revenues, particularly before it was sold to Swiss Bank Corporation (now part of UBS) in the summer of 1997, changing its name to SBC Warburg Dillon Read.

In the April 1997 Dillon Cornell SEC filing, the Concord Japan venture fund invested in Cornell is described as a corporation organized under the laws of the Bahamas, whose principal office and business address was c/o Roy West Trust Corporation, (Bahamas) Limited, West Bay Street, Nassau, Bahamas. Hence, Concord and Concord II were “onshore” funds and Concord Japan was an “offshore” fund. The officers and directors of Concord Japan include representatives of some of the largest most prestigious Japanese corporations as well as Amerex SA which listed its address as the Coutts Bank office in the Bahamas. Coutts is considered one of the most prestigious private banks in the world.[39] In May 1991, Dillon invested additional funds from one of the Lexington Funds.[40] The Lexington Funds were created to invest money for Dillon officers and directors. Dillon then made additional investments with these various funds in September and November 1991. By the time of Cornell’s initial public offering of stock in October 1996, Dillon Read and the funds it managed and its officers and directors had accumulated approximately 44% of the outstanding common stock. This meant that they were the controlling shareholders. Along the way, Dillon officers and directors had personally purchased significant shares of Cornell stock. Investors included Chairman John Birkelund, Vice Chairman Dave Niemiec who signed many of the documents on behalf of Dillon and Lexington, President and CEO Franklin “Fritz” W. Hobbs, IV as well as numerous other senior partners, including Ken Schmidt. Dillon officer Peter A. Liedel, who signed on behalf of Concord, had joined the board of Cornell. Cornell named one of its facilities after him — the Liedel Community Correctional Center, a pre-release facility in Houston.

Source: Cornell Corrections, Inc. April 1997 13-D Filing by Dillon Read. Note: For the full list of 32 Dillon officers with personal positions, click here.[41]

Dillon’s investments in Cornell represent an extraordinary firm-wide commitment to starting up one company. This was not a common occurrence, but as we will see, this was not the first time that Dillon Read had backed a Houston business involved in privatization in an extraordinary way. The decision for an officer and director to buy shares would have been an individual decision — whether they used their own funds or if the firm helped arrange credit or other funds for them to finance their purchases. Hence, this meant that a significant number of Dillon's leadership decided that investing was something they actively wanted to do and for which they chose to be financially and ethically liable. One can only wonder what the Dillon leadership had been led to believe about the future of the private prison business, let alone what it implied about the future of the country. |

Based on company SEC filings, Houston-based Cornell Corrections started off with correctional facilities in Massachusetts and Rhode Island in 1991 and then in 1994 acquired Eclectic Communications, the operator of 11 pre-release facilities in California with an aggregate design capacity of 979 beds. An important relationship for Cornell from the start was the U.S. Marshals Service, an agency of DOJ, who was Cornell’s primary client for its Donald W. Wyatt Federal Detention Facility in Central Falls, Rhode Island, a facility with a capacity of 302 beds.

An article by Jeff Gerth and Stephen Labaton in the New York Times in November 1995, 'Prisons for Profit: A Special Report; Jail Business Shows Its Weaknesses" describes the problems that Cornell ran into with its Rhode Island facility. This facility had been financed with municipal bonds issued through the Rhode Island Port Authority in the summer of 1992 and underwritten by Dillon Read. The article states:

Dillon Read had long standing relationships with Brown & Root and the Houston banking and business leadership as a result of the firm's historical role in underwriting oil and gas companies, including pipelines. In 1947, Herman and George Brown, the founders and owners of Brown & Root, were part of a group of Texas businessmen banked by Dillon Read as investor and underwriter (in a manner very similar to Dillon's backing of Houston-based Cornell many years later) to form the Texas Eastern Transmission Co. to buy the "Big Inch" and "Little Big Inch" pipelines in a privatization by the U.S. government. The Texas Eastern pipelines were critical to bringing natural gas from Texas and the Southwest to Eastern markets. For most Americans, Houston and New York seem far apart. However, the intimacy of their connection is better understood when you study the investment syndicates that controlled the railroad, canals, pipelines and other transportation systems that have connected these markets and helped to determine control of the local retail businesses for both goods and capital along the way. For example, Texas Eastern's Big Inch pipeline went from east Texas to Linden, New Jersey, some 30 miles away from the Dillon and Brady estates in New Jersey and approximately 20 miles from the Dillon Read offices on Wall Street. According to investigative journalist Dan Briody in The Halliburton Agenda: The Politics of Oil and Money, the Brown brothers netted $2.7 million in profits on their shares in their initial public offering right after the company was formed and won the bid to buy the pipelines from the government in the late 1940's. That, however, was not the real payoff. According to Briody, Brown & Root subsequently worked on 88 different jobs for Texas Eastern, and generated revenues of $1.3 billion from Texas Eastern between 1947 and 1984. [42.1] According to Robert Sobel in The Life and Times of Dillon Read, under August Belmont's personal leadership of the transaction, Dillon Read also made a profit on the Texas Eastern shares. "Nothing is known of Dillon Read's profits on the underwriting, but it was a sizeable owner of TETCO [Texas Eastern] common, acquired at 14 cents a share, which rose to $9.50." [42.2] While figures for Dillon Read revenues from underwriting and other investment banking services over the years comparable to Brown & Root's construction contracts are not available, my recollection was that Dillon continued to maintain a profitable relationship with Texas Eastern when I worked at the firm in the 1980s many decades later. Interestingly enough, Briody also describes in detail the McCarthyist efforts that were made to destroy Federal Power Commission chairman Leland Olds, an honest government official, because his ethical regulatory decisions threatened the richness of the Texas Eastern profits. The clear implication is that the pattern of generating financial windfalls from government privatizations combined with dirty tricks against honest government officials is nothing new. [42.3] The closeness of the Brown & Root relationship with Dillon Read is also underscored by Briody's description of the head of Brown & Root’s frustration with Lyndon Johnson's decision to serve as John Kennedy's running mate. He quotes August Belmont, by then a leader of Dillon Read, who was with Brown in Houston in his private hotel suite listening to the radio coverage of Johnson's announcement. According to Belmont, "Herman Brown....jumped up from his seat and said, 'Who told him he could do that?' and ran out of the room." [42.4] What Briody does not mention is allegations regarding Brown & Root's involvement in narcotics trafficking. Former LAPD narcotics investigator Mike Ruppert once described his break up with fiance Teddy — an agent dealing narcotics and weapons for the CIA while working with Brown & Root, as follows:

Another important relationship for the Houston-based Cornell Corrections was the California Department of Corrections. Whether this reflected that California was home base for David Cornell’s former employer, Bechtel, is not clear. When Cornell Corrections got started, California had the largest prison population of any U.S. governmental entity. In part due to extraordinary growth in incarcerations of non-violent drug users as a result of the War on Drugs, the federal prison population managed by the Federal Bureau of Prisons at the Department of Justice has become the largest with 186,560 based on their September 8, 2005 weekly update.[44] California is close behind with 168,000 youths and adults incarcerated in California prisons and 116,000 subject to parole.

Cornell’s Chief Financial Officer, Treasurer and Secretary was Steven W. Logan, who had served as an experienced manager in Arthur Anderson’s Houston office. This was the same office of Arthur Anderson that had served as Enron’s auditor until the Enron bankruptcy brought about the indictment and conviction of Arthur Andersen.[45] Arthur Andersen was Cornell’s auditor, having first served as a consultant to create market studies which helped support the approvals for and financing of the building of the Rhode Island facility for the U.S. Marshals Service. Logan was later forced out of Cornell after an off-balance sheet deal[46]engineered with the help of a former Dillon Read banker Joseph H. Torrence, like those done for Enron was called into question and significant stock value declines triggered litigation from shareholders.

Most venture capital investors prefer to exit their investment within 5 years. That means that Dillon Read would have likely wanted to establish or start their exit from Cornell by 1996. The stock market was hungry for Initial Pubic Offerings (IPOs) where a new company sells its stock to the public for the first time. Venture capitalists typically make their profit from financing a company and then selling their equity when a public market has been established for the company’s stock. However, by the end of 1995, Cornell’s story was not an exciting one. It was not a market leader, its growth was slow and it had no profits. If the calf was going to be taken to market, it would need fattening. A Note on “Prison Pop”The “pop” is a word I learned on Wall Street to describe the multiple of income at which a stock is valued by the stock market. So if a stock like Cornell Corrections trades at 15 times its income, that means for every $1 million of net income it makes, it's stock goes up $15 million. The company may make $1 million, but its “pop” is $15 million. Folks make money in the stock market from the stock going up. On Wall Street, it's all about “pop.” Prison stocks also are valued on a “per bed” basis — which is based on the number of beds provided and the profit per bed. “Per bed” is really a euphemism for people who are sentenced to be housed in their prison. For example, in 1996, when Cornell went public, based on the financial information provided in the offering document provided to investors, its stock was valued at $24,241 per bed. This means that for every contract Cornell got to house one prisoner, at that time, their stock went up in value by an average of $24,261. According to prevailing business school philosophy, this is the stock market’s current present value of the future flow of profit flows generated through the management of each prisoner. This, for example, is why longer mandatory sentences are worth so much to private prison stocks. A prisoner in jail for twenty years has a twenty-year cash flow associated with his incarceration, as opposed to one with a shorter sentence or one eligible for an early parole.[47] This means that we have created a significant number of private interests — investment firms, banks, attorneys, auditors, architects, construction firms, real estate developers, bankers, academics, investors among them— who have a vested interest in increasing the prison population and keeping people behind bars as long as possible. When you invest in stock, you make money if and when you sell the stock at a higher price than you paid for it. This would be true for the people who invested in Cornell stock, including Dillon Read and its venture funds. Cornell was run by a board of directors that represented the shareholders, particularly the controlling shareholders — in this case Dillon Read. The board is the group of people who decides what goes. Senior management officials, such as the founder and Chairman David Cornell, who run the company day to day, are also on the board. Most of the money they make comes from stock options that they get to encourage them to get the stock to go up for the investors. That means that what everyone who runs the company wants is for the stock to go up. There are two ways to make the stock go up. First, you can increase net income by increasing capacity — the number of “beds” — or profitability — “profits per bed.” Second, you can increase the multiple at which the stock trades by increasing the markets’ expectations of how many beds or what your profit per bed will be and by being very accessible to the widest group of investors. So, for example, passing laws regarding mandatory sentencing or other rules that will increase the needs for prison capacity can increase the value of private prison company stock without those companies getting additional contracts or business. The passage of — or anticipation of — a law that will increase the demand for private prisons is a “stock play” in and of itself. The winner in the global corporate game is the guy who has the most income running through the highest multiple stocks. He is the winning “pop player.” Like the guy who wins at monopoly because he buys up all the properties on the board, he can buy up the other companies. So the private prison company that wins is the one that gets the most contracts that guarantee it the most prisons and prisoners that generate the most income for the longest period with the smallest amount of risk. The way that Cornell could become a winner quickly was to get lots of government contracts to house lots of prisoners and acquire other companies with government contracts to house lots of prisoners and do it quickly.[48] And that was exactly what happened. |

|||||||||||||||||||||||||||||||||||||||||||||

The U.S. Marshals Service is the oldest U.S. enforcement agency. Among other duties, the U.S. Marshals Service houses and transports prisoners prior to sentencing and provides protection for the federal court system. According to the Marshals Service’s website, they are also:

The U.S. Marshals Service is the oldest U.S. enforcement agency. Among other duties, the U.S. Marshals Service houses and transports prisoners prior to sentencing and provides protection for the federal court system. According to the Marshals Service’s website, they are also:

Cornell’s early years of business were not financially profitable. The private prison industry faced significant resistance and legal and operational challenges to privatizing federal, state and local prison capacity. Within the private prison industry, Cornell faced competition for new contracts and acquisitions from two larger, more experienced companies, CCA and Wackenhut. By 1995, compared to industry leaders, Florida-based Wackenhut and Tennessee based Corrections Corporation of America (CCA), Cornell Corrections appeared to be lagging in government contract growth. As of mid 1996, Cornell was carrying $8 million of cumulative losses on its balance sheet.

Cornell’s early years of business were not financially profitable. The private prison industry faced significant resistance and legal and operational challenges to privatizing federal, state and local prison capacity. Within the private prison industry, Cornell faced competition for new contracts and acquisitions from two larger, more experienced companies, CCA and Wackenhut. By 1995, compared to industry leaders, Florida-based Wackenhut and Tennessee based Corrections Corporation of America (CCA), Cornell Corrections appeared to be lagging in government contract growth. As of mid 1996, Cornell was carrying $8 million of cumulative losses on its balance sheet.

Much has been written about the use of the War on Drugs to intentionally disenfranchise poor people and engineer the centralization of political and economic power in the U.S. and globally, including an explosive rise in the U.S. prison population. The purpose of this story is not to repeat this fundamentally sound thesis. For those who are interested in more on this topic, I would refer you to my article and audio seminar “Narco Dollars for Beginners” as well as Michael Woodiwiss’ book Organized Crime and American Power (University of Toronto Press, 2001) and their associated bibliographies.[49]

The Clinton Administration took the groundwork laid by Nixon, Reagan and Bush and embraced and blossomed the expansion and promotion of federal support for police, enforcement and the War on Drugs with a passion that was hard to understand unless and until you realized that the American financial system was deeply dependent on attracting an estimated $500 billion-$1 trillion of annual money laundering. Globalizing corporations and deepening deficits and housing bubbles required attracting vast amounts of capital.

Attracting capital also required making the world safe for the reinvestment of the profits of organized crime and the war machine. Without growing organized crime and military activities through government budgets and contracts, the economy would stop centralizing. The Clinton Administration was to govern a doubling of the federal prison population.[50] Whether through subsidy, credit and asset forfeiture kickbacks to state and local government or increased laws, regulations and federal sentencing and imprisonment, the supremacy of the federal enforcement infrastructure and the industry it feeds was to be a Clinton legacy. One of the first major initiatives by President Bill Clinton was the Omnibus Crime Bill, signed into law in September 1994. This legislation implemented mandatory sentencing, authorized $10.5 billion to fund prison construction that mandatory sentencing would help require, loosened the rules on allowing federal asset forfeiture teams to keep and spend the money their operations made from seizing assets, and provided federal monies for local police. The legislation also provided a variety of pork for a Clinton Administration vogue constituency — Community Development Corporations (CDCs) and Community Development Financial Institutions (CDFIs). The CDCs and CDFIs became instrumental during this period in putting a socially acceptable face on increasing central control of local finance and shutting off equity capital to small business. The potential impact on the private prison industry was significant. With the bill only through the house, former Attorney General Benjamin Civiletti joined the board of Wackenhut Corrections, which went public in July 1994 with an initial public offering of 2.2 million shares. By the end of 1998, Wackenhut’s stock market value had increased almost ten times. When I visited their website at that time it offered a feature that flashed the number of beds they owned and managed. The number increased as I was watching it — the prison business was growing that fast. However, the Clinton Administration did not wait for the Omnibus Crime Bill to build the federal enforcement infrastructure. Government-wide, agencies were encouraged to cash in on support in both Executive Branch and Congress for authorizations and programs — many justified under the umbrella of the War on Drugs — that allowed agency personnel to carry weapons, make arrests and generate revenues from money makers such as civil money penalties and asset forfeitures and seizures. Indeed, federal enforcement was moving towards a model that some would call “for profit” faster than one could say “Sheriff of Nottingham.”